KUALA LUMPUR 30 Dis The government has agreed to exempt taxation on foreign source income FSI for resident taxpayers to ensure the smooth implementation of the tax initiative said the Ministry of Finance MoF. Foreign dividend withholding tax suffered would be creditable against Malaysian tax payable.

How To Report Foreign Earned Income On Your Us Tax Return

The categories of foreign-sourced income that are exempt from income tax are the following.

. January 7 2022. One of the most significant proposed changes to our tax system is imposition of tax on foreign sourced income. Such income will be treated equally vis-à-vis income accruing in or derived from Malaysia and taxable under Section 3 of the ITA.

Malaysia only taxes income that arises in Malaysia. Based on the 2004 assessment year effect a foreign-sourced income. Foreign-sourced income is chargeable to tax under Section 3 of the Income Tax Act 1967.

Impact on companies. The tax exemption is effective from Jan 1 2022 to Dec 31 2026. In summary the tax treatments for income of a.

However this exemption will cease to apply with effect from 1 January 2022. The tax would be imposed at a transitional tax rate of 3 based on the gross amount received from 1 January 2022 through 30 June 2022. Published on 21 January 2022 reading time approx.

With the withdrawal of the tax exemption beginning 1 January 2022 foreign-sourced income received in Malaysia by any Malaysian resident person will be subject to tax. All types of income received by individual taxpayers. Section 3 of the Income Tax Act 1967 ITA states that income shall be charged for the income of any person accruing in or derived from Malaysia or received in Malaysia from outside MalaysiaThe phrase accruing in or derive from Malaysia means the source of income must be in Malaysia.

The following foreign-sourced income received will continue to be exempted from Malaysian income tax from 1 January 2022 to 31 December 2026 5 years. Section 3 Income Tax Act 1967 ITA says that income shall be charged for the income of any person accruing in or derived from Malaysia or received in or from Malaysia. With effect from YA 2004 foreign source income derived from sources.

The Inland Revenue Board issued a media release about. The income tax exemption is effective from January 1 2022 until December 31 2026. 1 2022 the current income tax exemption on foreign-sourced income FSI received in Malaysia by Malaysian residents will be removed.

How about capital gain in foreign country remitted to. For years some foreign sourced income had fallen under tax exemption in Malaysia effectively reducing the taxable income of some Malaysian citizens working abroad and sending money home. Subject to Inland Revenue Board criteria and guidelines.

It has been given a tax exemption since YA 2004. KTP takeaways There are questions to be answered. Such income was taxed prior to the year of assessment 1995.

There will be a transitional period from 1 January 2022 to 30 June 2022 where FSI remitted to Malaysia will be taxed. Income is taxed whilst capital is not. Certain tax treaties allow foreign tax paid by the subsidiary companies in respect of their income.

Foreign sourced income received in Malaysia will be taxed effective January 1 2022. November 18 2021. This is a significant overhaul to our taxation system which has been predominantly a territorial tax system.

2 minutes Under the Budget 2022 proposal the Malaysian Government proposed to remove the exemption of Foreign Sourced Income FSI received by any person other than a resident company carrying on business in banking insurance or seaair transport which has been provided under Paragraph 28. The transitional period from 1122 to 30622 whereby foreign source income remitted to Malaysia is taxed at 3 on gross income. The Finance Ministry in late December 2021 extended through 31 December 2026 a tax exemption available for foreign-source income for individuals and foreign-source dividend income for corporate taxpayers subject to certain conditions.

The phrase accrues in or from Malaysia tells to that the income source should be from Malaysia. Dividends received by companies and limited liability partnerships. Taxation of foreign source income is not new to Malaysia.

With effect from Jan. This article published in the Tax Guardian January 2022 issue by KPMGs. However Section 27 of the Finance Act 2021 amended paragraph 28 of Schedule 6 to read as follows.

Once the amendments to the Income Tax Act are passed foreign sourced income that is remitted to Malaysia by Malaysian residents individuals and corporates would be subject to tax starting from 1 January 2022. While we expect the Inland Revenue. Prior to December 31 2021 paragraph 28 of Schedule 6 provided that foreign source income received in Malaysia by an individual or company carrying out business other than banking insurance or sea or air transport is exempt from income tax.

This is in response to global developments such as the global minimum tax and the recent European Union action to include Malaysia in its grey list. Dividends received by Malaysian resident companies from foreign subsidiaries would be taxed in Malaysia with effect from Jan 1 2022. From 1722 any foreign source income remitted to Malaysia will be subjected to the current prevailing rate.

THE government has made a surprising U-turn on Dec 30 2021 after announcing that foreign-sourced income received in Malaysia by Malaysian tax residents will be taxed. In the most recent budget which was announced in October 2021 it was stated that from January 2022 the treatment of foreign sourced income would be changing. The Chartered Tax Institute of Malaysia.

Income vs capital The first hurdle to cross is to determine whether the monies remitted into Malaysia is income or capital. This article highlights the impact and practical considerations that businesses and individuals alike should contemplate in preparing for the impending tax on FSI. For many years Malaysian resident companies individuals and unit trusts amongst others have enjoyed a general exemption for foreign source income.

Effectively income tax will be imposed on resident persons in Malaysia on income derived from foreign sources and received in Malaysia with effect from 1 January 2022. In the 2022 Budget announcement it is proposed that with effect from 1 January 2022 foreign-sourced income FSI of Malaysian tax residents both companies and individuals which is received in Malaysia will be subject to tax. A provision in the Finance Bill would tax foreign-source income received by any Malaysian resident person effective from 1 January 2022.

The relief is provided in response to the coronavirus COVID-19 pandemic.

Taxation Of Investment Income Within A Corporation Manulife Investment Management

![]()

Guide To Tax Clearance In Malaysia For Expatriates And Locals Toughnickel

![]()

Tax Implications On Money Transferred From Abroad To India Extravelmoney

Countries With Zero Foreign Income Tax Youtube

Top 8 Countries With No Income Tax That You Should Know

Tax Alert Grant Thornton Malaysia

8 Countries With Zero Foreign Income Tax

8 Countries With Zero Foreign Income Tax

Foreign Income Tax Malaysia Removal Of Exemptions

How Much Foreign Income Is Tax Free In Canada Cloudtax Simple Tax Application

Kpmg Malaysia

4 Ways To Reduce Your Taxes On Your Foreign Income

Foreign Companies Expat Tax Professionals

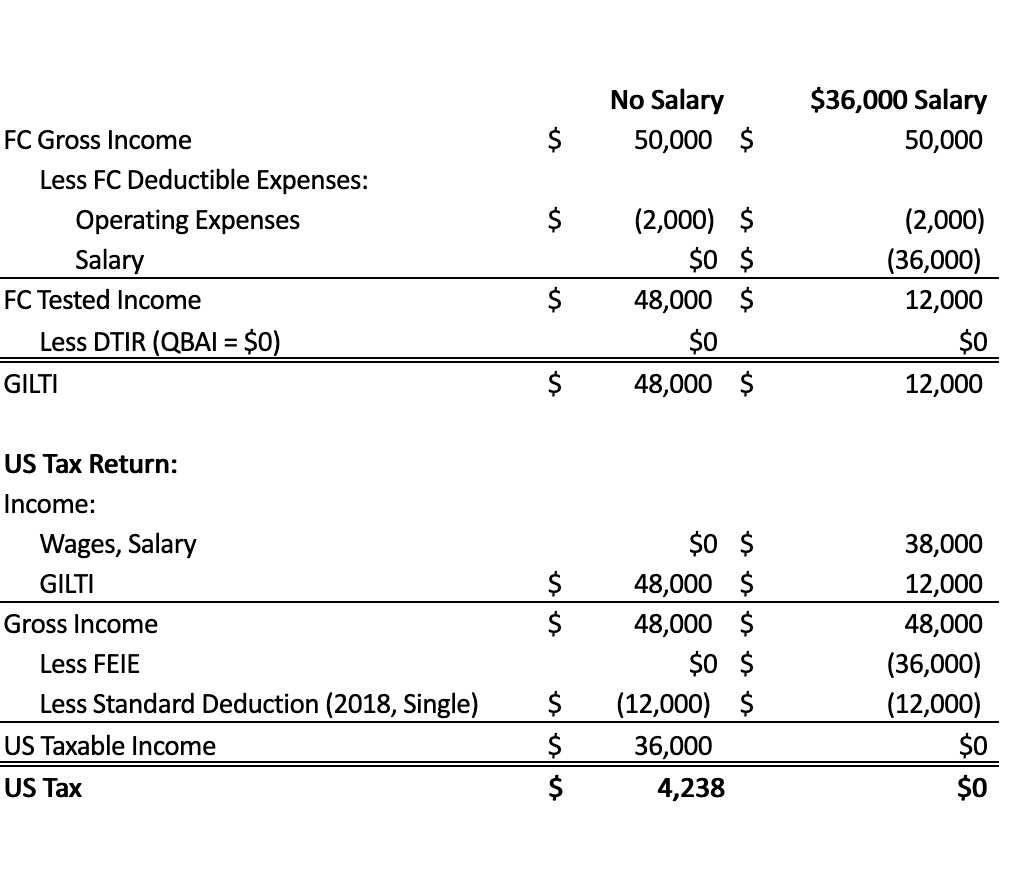

Getting To Know Gilti A Guide For American Expat Entrepreneurs

Thailand Income Tax For Foreigners Do You Need To Pay

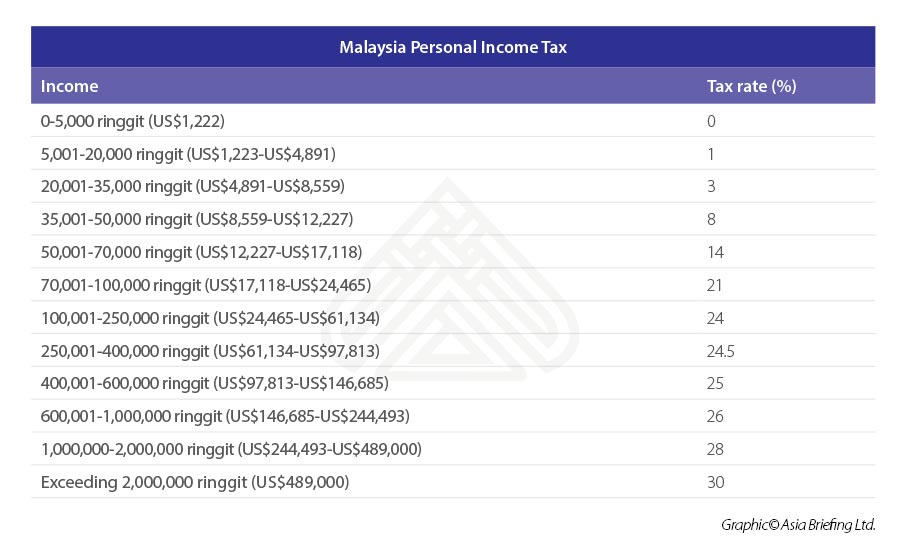

Individual Income Tax In Malaysia For Expatriates

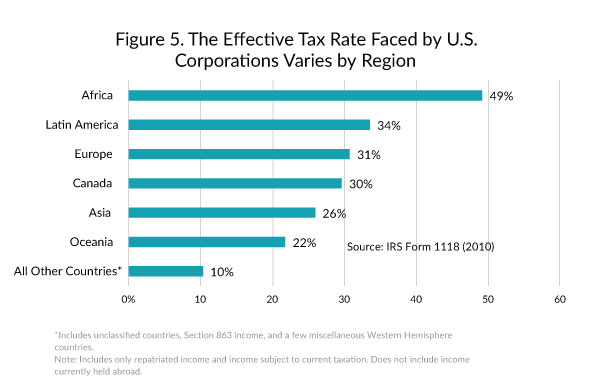

How Much Do U S Multinational Corporations Pay In Foreign Income Taxes Tax Foundation

Malaysia Issues Tax Exemption For Foreign Sourced Income

Is Foreign Income Taxable